Serving the community since 1970

Serving the community since 1970

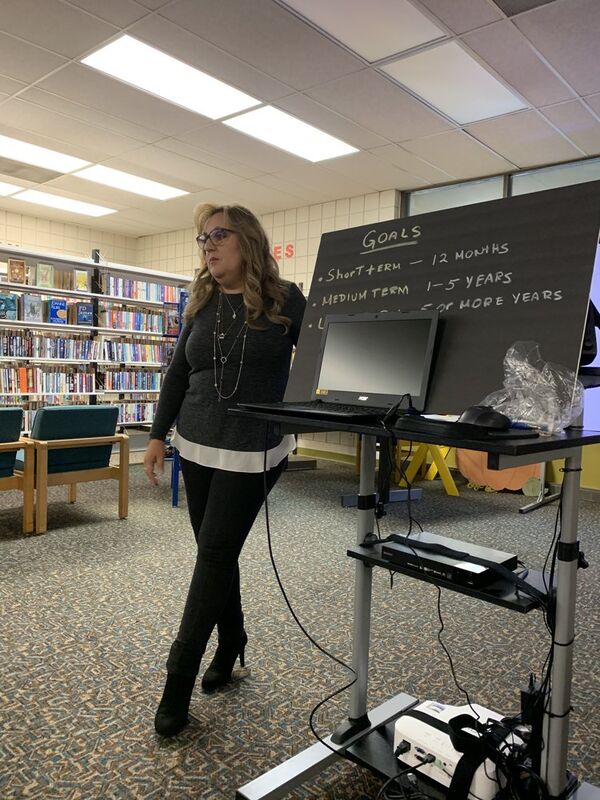

Ruth Ramos, Financial Foundation workshop presenter.

A local business leader gave a workshop on financial planning goals to start off 2020.

Ruth Yazmin Ramos of State Farm held a workshop at the Wasco branch library Saturday and walked participants through a worksheet with advice on how to begin financial planning for the upcoming year.

Ramos's first words emphasized how important it is to set goals.

Goal setting encompasses three stages. They are

--Short-term goals (purchases within the next 12 months),

--Medium-term goals (future purchases within 1-5 years)

--Long-term goals (future purchases in 5 or more years)

Short-term goals could be for the purchase of a new appliance, pay off or pay down a debt or save money for something coming up in the near future (such as vacation, car repair, etc.). A medium-term goal could include saving for a new car, and saving for retirement. Ramos stated that a long-term goal could also be used as methods to save for retirement (depending on your age), purchasing CDs or joining a money market account at financial institution or bank.

"You should not have your medium-term or long-term goal money where you can take it out on a regular basis by using a debit card, Ramos suggests. "That money should not be available for easy removal. It's meant as a savings tool."

Ramos stated that setting goals is an important first step because goals are the basis for spending and savings plan (i.e. your budget).

The second part of the workshop was to build a budget. "Everyone should have a budget and know what they bring in each month and pay out each month," she added. "Building a budget will put you in control of your money by telling your money where you want it to go, rather than wondering where it went."

Under a budget there are fixed expenses such as mortgage or rent, phone, cable/internet, utilities, home insurance, renters insurance, life insurance, gardener, car loan and student loan, as well as any monthly credit cards you have to pay.

The next category is variable expenses such as groceries (where the amount changes each month), entertainment, dining out, clothing and laundry.

The last category included nonmonthly expenses such as car maintenance, home maintenance, gifts and holidays.

She had everyone add up their fixed expenses, variable expenses and nonmonthly expenses and add up their total income, then subtract their total expenses to come up with disposable income.

Part 3 of the workshop was about saving money. "Your disposable income (the money you have left over each month is what you'll use to put towards your savings goals," Ramos stated.

She also said that since it can be tempting to dip into your savings if it's directly connected to your main checking account, consider opening a separate savings account with another agency to help prevent that temptation.

Savings for an emergency fund and retirement goal 1 (short-term goals) and goal 2 (medium to long-term goals) is how the disposable income should be divided.

"Everyone should save at least 10 percent of their gross income each month," Ramos said.

The fourth area she discussed was managing debt. "Managing debt is all about finding a balance between building your savings and paying down your debt," Ramos said. "The best way to start prioritizing your debt is to write them all down along with their balance and interest rates."

Ramos described two kinds of debt -- good debt and bad debt. Good debt has generally lower interest rates, grows in value or generates long-term income (i.e., mortgages, etc., and in some cases purchasing a vehicle).

"Even though once a new vehicle is driven off the lot [and] it depreciates in value immediately, if you use the vehicle to get to a job where you earn money to live, that could be considered a good debt," Ramos said. "On the other hand, if you purchase a vehicle and you are retired and don't drive much, that could be considered a bad debt."

A bad debt is one that has higher interest rates and doesn't provide any future value (i.e. credit cards, private loans, etc.)

She also stated that one of the more important factors in debt is how regularly you pay your debt back. If you are regular on your payments and pay more than the minimum due, your debt will dissolve quicker than if you pay the minimum amount due.

A credit score is calculated by the following criteria:

--35% :Do you pay your bills on time?

--30%: Do you have low balances on your credit cards or are they maxed out?

--15%: Length of credit history. Have you been building your credit for a long time or did you just start?

--10%: Credit mix. Do you have both types of credit including installment (this has an end date) and revolving (has no end date).

--10%: Credit inquiries: Have you recently applied for credit or has it been a while?

Anyone interested in a financial foundation workshop is invited to contact Ramos at 661-758-5164. She also is available for individual consultations.

Reader Comments(0)